Recording of Tuesday, May 06, 2025 | The smarter E Europe Conferences | Conference Program | Language: English | Duration: 18:23 .

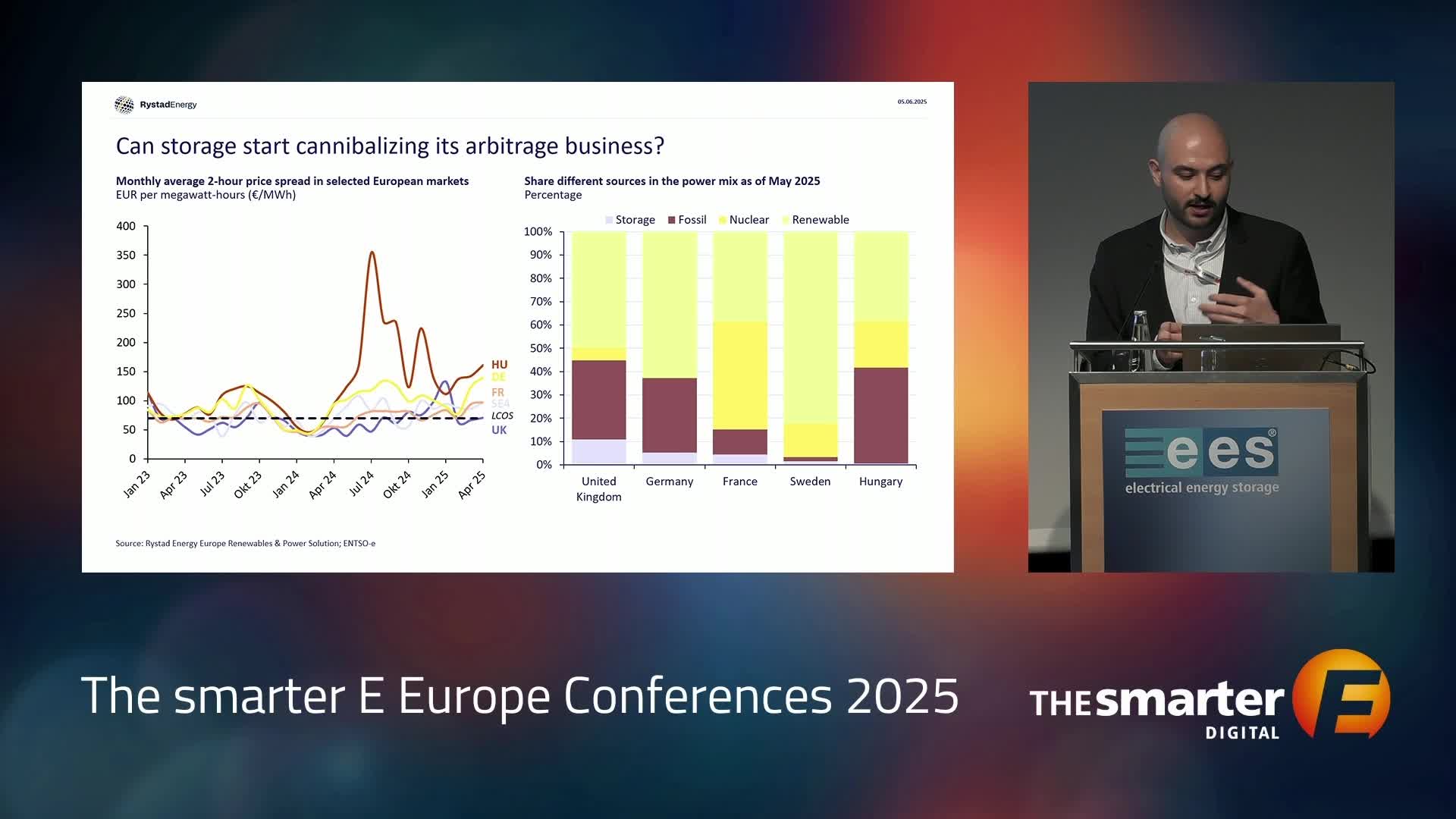

The presentation explores the energy trading spot market, emphasizing batteries as a key revenue source. Rystad Energy provides insights into this sector through its comprehensive data analytics approach. The focus is on Europe's transition to renewables such as solar and wind, which accounted for 25% of generated electricity last year and are expected to exceed 50% by 2035. This shift will require enhanced battery storage flexibility. In China’s competitive DC block system market, bids now range from $200 down to below $50 per kilowatt-hour, with intense competition driving some players toward negative margins. Globally, technological advancements have reduced battery project capex below $300/kWh while extending cycle life to over ten years or more than 10,000 cycles. As a result, the levelized cost of storage (LCOS) is now around €90/MWh when cycled daily—a notable decrease from previous costs of about €140/MWh just two or three years ago. This is now closely aligned with current European power prices, enabling profitable business cases through strategic cycling and adaptation to evolving PPA trends. Contracted agreements have recently doubled, indicating growing interest despite earlier challenges in this field. Energy trading dynamics highlight the high-risk/high-return potential of merchant revenues, in contrast to the more stable long-term income from contracted revenues, which is beneficial for project financing. In 2023, average revenue was about €120/MWh, with projections increasing as the share of renewables continues to rise. Developers tend to benefit more than producers, mainly due to increased market volatility creating arbitrage opportunities. For example, Hungary’s limited capacity causes significant price fluctuations, while saturated markets like the UK see flatter profits due to widespread utility-scale installations and negatively priced excess production during periods of inflexible nuclear baseload. Operators who can effectively manage these volatile environments are expected to benefit at least until the mid-2020s, with lucrative possibilities in regions like Germany and Hungary, though payback periods will vary based on capex levels (e.g., $250 vs. $200/kWh). Enhancing the business case increasingly involves incorporating ancillary services, with emerging concepts like virtual inertia. However, quantifying these benefits remains challenging due to forecasting limitations and the future evolution of pricing and control markets. Kronos software was mentioned in the German context for its simulation capabilities, including scheduling phases, dispatch optimization, and additional signals for selection rate estimation and share capture, all informed by historical bid data. Dries Acker from Solar Power Europe highlighted the political underrepresentation of battery storage at the EU level. He noted that the EU has now introduced an advocacy initiative—the Battery Storage Platform—to bolster support and realize the full projected benefits of battery storage.

Automated summarization by AI Conver

Sepehr Soltani

Senior Analyst

Rystad Energy

Norway

What are emerging trends in battery storage? How are installation numbers evolving across the residential, C&I, and utility-scale battery markets? What new and existing applications are driving market growth? What can we learn from developments in other regions, such as the UK, and what insights can be applied to the European market? These are the questions that will be explored in this session.

Further Talks of this session:

Speaker

Dr. Alexander Hirnet

Vice President Device Development

sonnen GmbH

Germany

Speaker

Antonio Arruebo

Market Analyst

SolarPower Europe

Belgium

Speaker

Anna Darmani

Principal Analyst, Energy Storage Europe

Wood Mackenzie

United Kingdom

Speaker

Simon De Clercq

Senior Associate

Aurora Energy Research

Germany