Recording of Monday, June 22, 2026 | The smarter E Europe Conferences 2026 | Language: English | Duration: 10:34 .

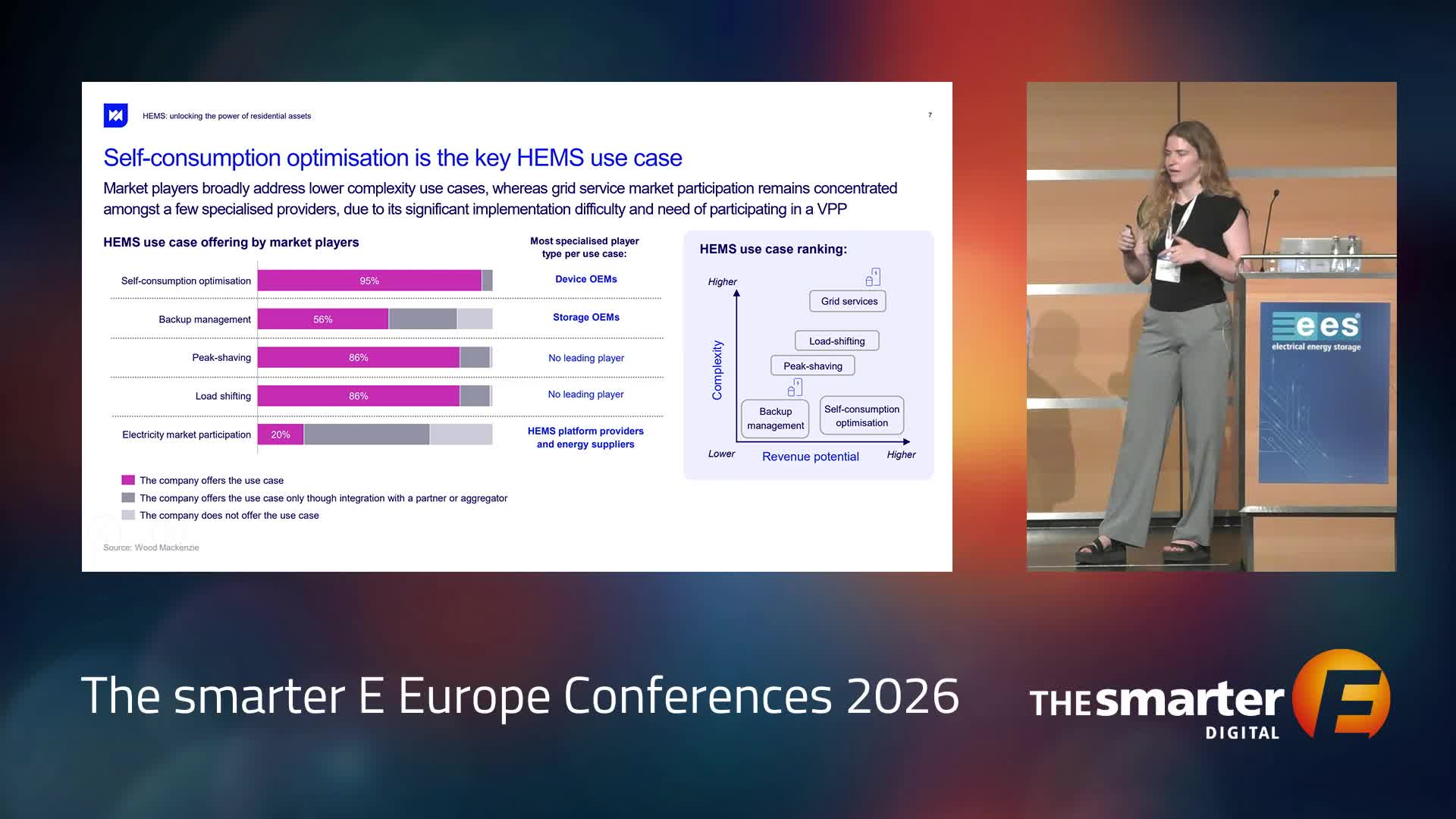

Home Energy Management Systems (HEMS) are digital solutions that optimize energy flow in homes, including generation, storage, consumption, and interactions with the grid. These systems can be delivered through various formats, such as standalone hardware, software, embedded devices, or hybrid setups. The adoption of HEMS is driven by the increasing prevalence of distributed energy resources, notably heat pumps, photovoltaic systems, electric vehicle chargers, and energy storage, with surging installations expected in the coming decade. Electrification trends show that energy demand in households significantly increases with electric vehicle and heat pump integration, with consumption rising by 60% and 81% respectively. Northern and western Europe show a favorable environment for HEMS adoption, influenced by distributed energy resource penetration and tariff structures. Key uses for HEMS include self-consumption optimization, backup management, peak shaving, load shifting, and electricity market participation. While self-consumption optimization is the most accessible and profitable, other use cases present varying degrees of complexity and revenue potential. Nevertheless, challenges such as slow smart meter implementation and customer reluctance towards dynamic tariffs hinder broader adoption.

Automated summarization by AI Conver

Speaker

Isabel Nieto Tous

Research Analyst

Wood Mackenzie

United Kingdom

The decentralized energy transition is entering a new phase: moving away from fixed feed-in tariffs toward market-based solutions and intelligent grid integration. In this context, Home Energy Management Systems (HEMS) combined with residential energy storage, are evolving from convenience and optimization tools into critical enablers of prosumer profitability. Opportunities arise from enhanced self-consumption optimization and the growing relevance of front-of-the-meter use cases such as direct marketing. However, challenges loom: a potential slowdown in new PV and residential storage installations and intensifying competition between large national installer platforms, independent HEMS-only players and OEMs in an increasingly crowded market. This session will analyze emerging business models, the competitive landscape and key success factors for HEMS providers in this pivotal market shift.

Further Talks of this session:

Speaker

Florian Mayr

Partner

Strategy&, part of the PwC Network

Speaker